Many Americans want a simple way to manage money without making budgeting feel complicated. The 50/30/20 Budget Rule is one of the most popular methods because it gives a clear structure: spend on needs, enjoy your wants, and save consistently. In 2025, the rule still works, but rising living costs, higher rent, and everyday inflation mean many people need to adjust it to fit modern financial life. This guide explains how the rule works, how to use it today, and what to change if your paycheck no longer stretches like it used to. Throughout this guide, the focus stays on practical steps anyone can apply. Since Right Paydays helps readers make smarter money choices, this framework supports better day-to-day financial control.

What the 50/30/20 Budget Rule Means

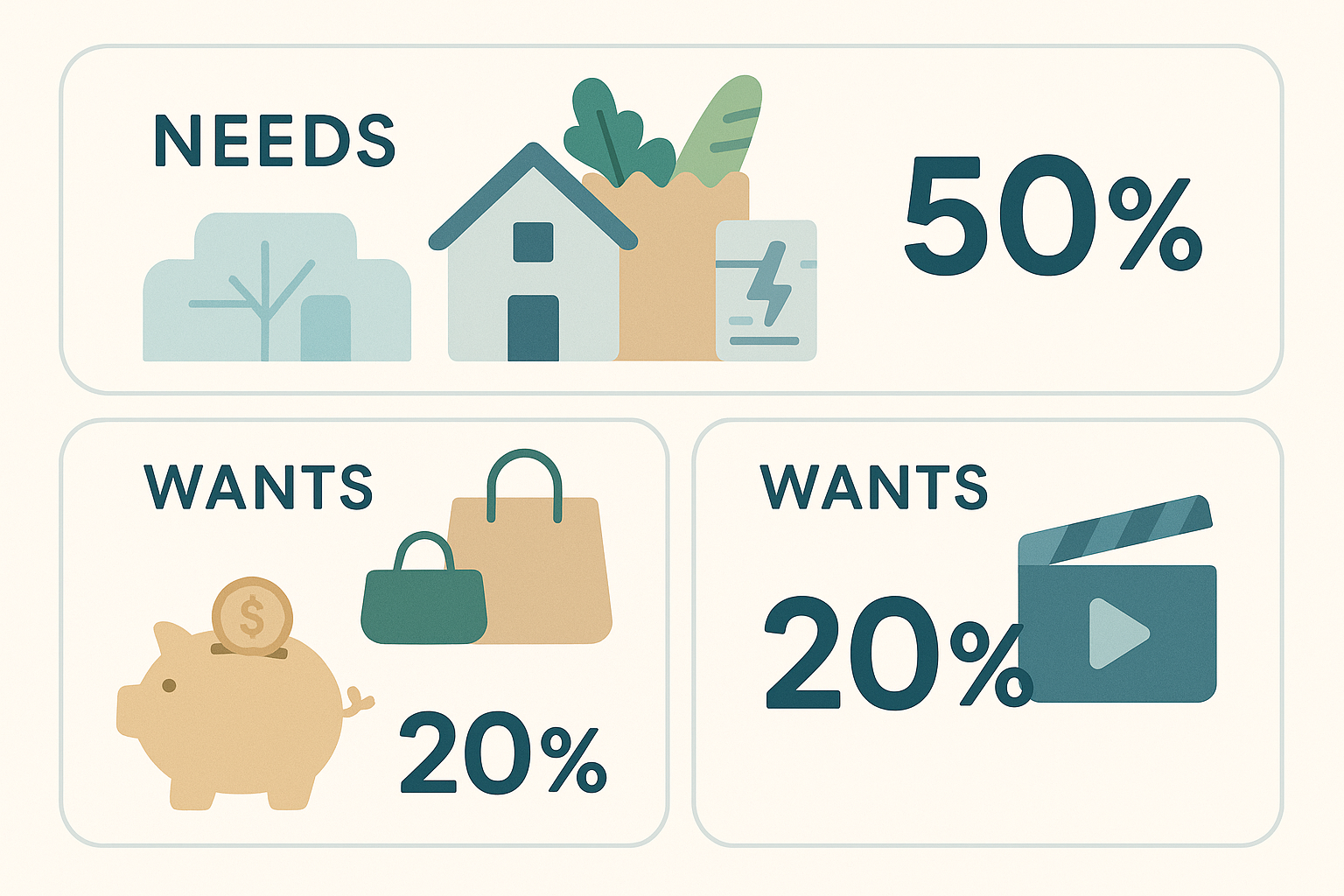

The 50/30/20 Budget Rule breaks your monthly take-home pay into three categories:

-

50 percent on needs

-

30 percent on wants

-

20 percent on savings and debt payoff

It is designed for beginners who want a clear, simple plan. The rule works because it avoids overtracking every dollar while still giving structure.

Needs (50 percent)

Housing, utilities, groceries, insurance, transportation, minimum loan payments, essential childcare. Anything required for basic living.

Wants (30 percent)

Dining out, entertainment, vacations, subscriptions, hobbies, shopping, tech upgrades, and nonessential lifestyle choices.

Savings and debt payoff (20 percent)

Emergency fund, 401(k), Roth IRA, sinking funds, extra debt payments, and short-term financial goals.

This breakdown works well for many people, but the rising cost of housing and medical expenses in the US often makes the 50 percent needs limit difficult. This is where flexible adjustments come in.

Does the 50/30/20 Budget Rule Still Work in 2025?

The rule still provides a strong starting point, but many Americans must adjust the percentages. Factors like higher rents, expensive groceries, credit card interest, and unexpected monthly fees can make the classic split unrealistic. The good news is that the 50/30/20 Budget Rule is a framework, not a strict law.

Most people today use one of these adjustments:

-

60/20/20: When rent or car payments leave less room for wants.

-

70/20/10: For households with high fixed expenses.

-

50/20/30: When savings need to be prioritized for a major goal.

-

40/30/30: For those wanting more lifestyle flexibility without losing savings discipline.

Right Paydays readers, especially those working on building emergency funds or reducing borrowing, often prefer a slightly higher savings percentage. The rule is effective if you adjust it to match your income, location, and lifestyle.

How to Start Using the 50/30/20 Budget Rule Step by Step

A beginner can set this up in less than an hour. The steps are simple.

Step 1: Calculate Your Monthly Take-Home Pay

Use net pay, not gross. Only count what arrives in your bank after taxes and deductions.

Step 2: Multiply Your Income by the Rule

Example if you earn $3,800 per month after taxes:

-

50 percent for needs: $1,900

-

30 percent for wants: $1,140

-

20 percent for savings: $760

This tells you how much room you have per category.

Step 3: List Your Actual Needs First

Write down rent, utilities, groceries, gas, insurance, and other essential bills.

If your needs exceed 50 percent, adjust your percentages. It is normal.

Step 4: Choose a Savings Priority

The 20 percent bucket can include:

-

Emergency fund

-

Retirement

-

Short-term savings goals

-

Credit card payoff

-

Sinking funds (annual bills, holidays, maintenance)

Step 5: Track Weekly Instead of Daily

Daily tracking overwhelms people. A weekly check-in works better and keeps spending under control without stress.

What Counts as a Need vs a Want?

This is one of the most confusing parts of the 50/30/20 Budget Rule.

Needs include:

Rent, essential utilities, medication, groceries, internet for work or school, transportation, insurance, and minimum payments on loans.

Wants include:

Dining out, premium grocery brands, gadgets, new clothes, Uber when you could use public transit, subscriptions, memberships, and entertainment.

A useful rule:

If you can survive without it, it is a want.

Money-Saving Strategies That Make the Rule Easier in 2025

These practical habits help keep spending stable even when prices rise.

Lower your fixed expenses where possible

-

Negotiate internet and phone plans

-

Switch to a cheaper insurance provider

-

Compare grocery prices at different stores

-

Refinance or consolidate high-interest debts if eligible

Cut wants without feeling restricted

-

Use cash envelopes for dining out or shopping

-

Cancel unused subscriptions

-

Reduce impulsive purchases by delaying them 24 hours

-

Choose free entertainment options more often

Build savings automatically

-

Automate transfers to savings every payday

-

Use accounts that separate emergency funds from regular savings

-

Take advantage of employer 401(k) match

-

Use sinking funds to prevent future debt

Use the right tools

Apps, banking features, or Right Paydays budgeting guides help track spending and improve awareness. Even simple spreadsheets work well.

Common Mistakes People Make With the 50/30/20 Budget Rule

Avoid these problems that affect many beginners:

-

Treating wants as needs

-

Ignoring rising subscription costs

-

Not adjusting the percentages to match income

-

Saving only what is left rather than saving first

-

Forgetting irregular expenses such as annual insurance

-

Underestimating grocery spending

-

Not reviewing the budget monthly

A budget is a living plan, not a one-time calculation. Adjust it whenever your income or expenses change.

When the 50/30/20 Budget Rule Doesn’t Work

Some readers may need a different method:

-

Income is extremely variable

-

Rent takes more than half your income

-

You live in a high-cost city

-

You are recovering from debt

-

You are saving aggressively for a short-term goal

In these cases, use the rule as a starting point but switch to a flexible version such as 60/30/10 or 70/20/10.

FAQs

What is the 50/30/20 Budget Rule in simple words?

It is a budgeting method that splits your take-home pay into needs, wants, and savings.

Is the 50/30/20 Budget Rule realistic for the US today?

Yes, but many people adjust it because of high housing, groceries, and transportation expenses.

Can I use the 50/30/20 Budget Rule if my income changes every month?

Yes. Use monthly averages or apply percentages to each paycheck individually.

Is the 50/30/20 Budget Rule good for beginners?

It is one of the easiest starting points because it avoids overtracking and gives clear limits.

How do I follow the 50/30/20 Budget Rule if my rent is too high?

Adjust the percentages, reduce wants, and grow income where possible. Many people follow versions like 60/20/20 or 70/20/10.

Can this rule help me build an emergency fund?

Yes. The savings category covers emergency fund contributions. It works well with guidance from Right Paydays.

Final Summary

The 50/30/20 Budget Rule remains a simple and effective way for Americans to manage money in 2025. It gives structure without complexity and helps control spending, plan savings, and handle rising costs more confidently. The key is flexibility. If the traditional 50/30/20 split doesn’t fit your income or lifestyle, adjust it to a version that works for you. With the right balance, this method supports better financial habits and builds long-term stability.

Take Part in Quiz & Win Points!

Challenge yourself and earn 10 points for every correct answer